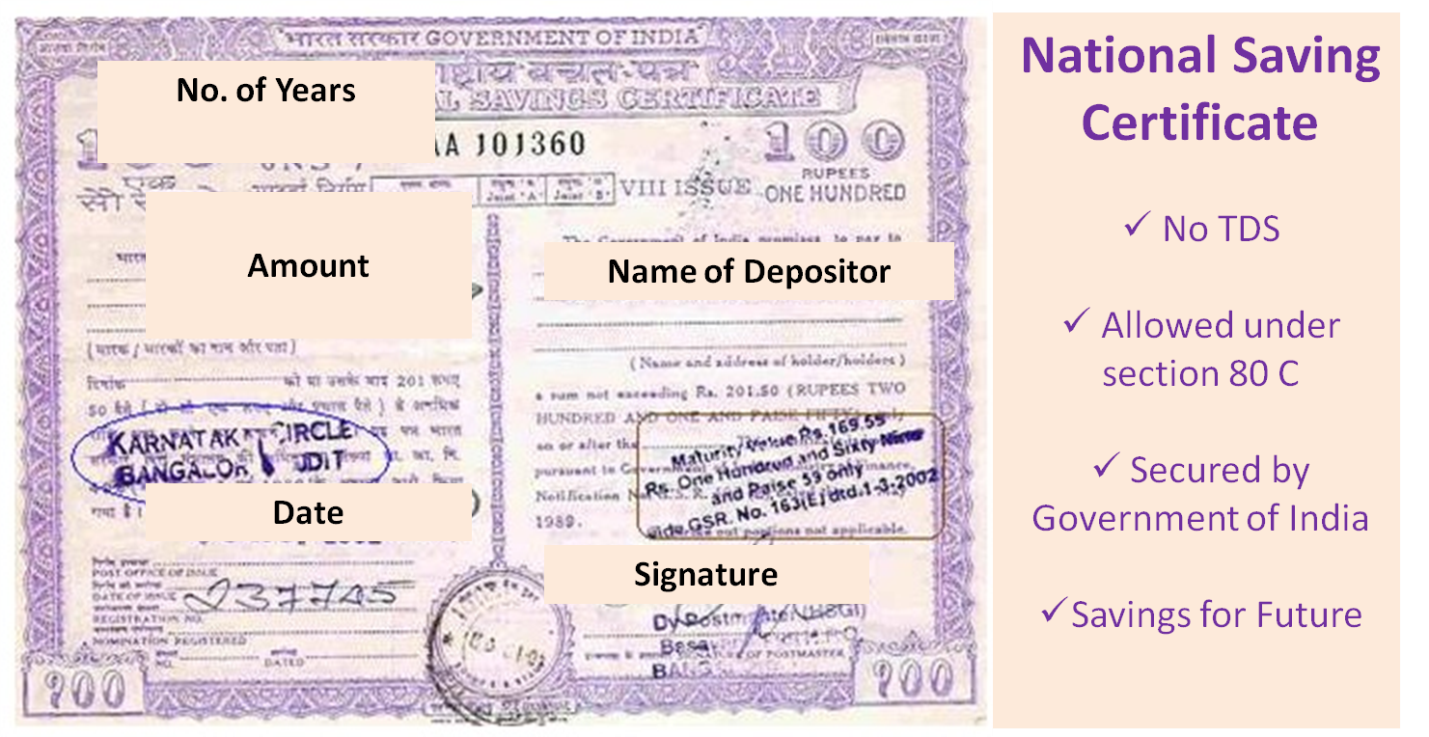

The National Savings Certificate (NSC) is a Government of India initiative that is easily accessible at any post-office. It is a fixed income tax-saving investment tool. It encourages individuals with small to mid-income range to invest and save tax under Section 80C.

NSC post office scheme is mainly chosen by people with low-risk tolerance and those who are looking for a fixed return instrument. If you are someone who wants to invest in NSC, then this article will guide you through all aspects of NSC: namely the benefits, features, interest rates, buying procedure of NSC, and even more. Read this page until the end to be able to make a well-informed decision about the NSC certificate.

What is a National Savings Certificate?

National Savings Certificate, abbreviated as NSC, is a type of Indian Government Savings bond that is usually used as small to mid-savings investments and income tax saving investments. You can open this kind of investment at any post office as it is a Government of India initiative. It is a secure and low-risk investment product. You can purchase it in your name, for a minor, or as a joint account with another adult.

Some details about the National Savings Certificate (NSC) are as follows:

- Maturity Period: 5 years (fixed)

- Interest Rate: currently 6.8% p.a. (fixed)

- Minimum investment: INR 100

- Maximum limit: Does not exist

- Tax Benefits: You will earn tax benefits under Section 80C of the IT Act only for investments up to INR 1.5 lakhs.

- TDS: No

- Mode of investment: Single, Joint “A”, Joint “B”

Image Source: expertmile.com

Who Should Invest in NSC?

If you are someone who wants a safe investment tool to save taxes and earn a steady income at the same time, then NSC is the right option for you.

NSC post office will give you a fixed interest and your investment capital stays protection. But, they do not provide inflation-beating returns like other tax-saving schemes like the tax-saving mutual funds and the National Pension System (NPS).

This is a savings scheme for individuals and is easily accessible as it is available at your nearest post office.

Who cannot invest in NSC?

Hindu Undivided Families (HUFs) and trusts, and non-resident Indians (NRIs) cannot invest in NSCs. This scheme is only for individual Indian citizens. The following list of people cannot invest in NSC:

- Hindu Undivided Families (HUFs)

- Trusts

- Private and public limited companies

- Non-Resident Indians (NRIs)

Eligibility for National Savings Certificate

Given below are the main eligibility criteria for National Savings Certificate investments:

- All Indian residents are eligible.

- NRIs are not eligible to buy new NSCs. But, if someone had purchased an NSC while residing in India, before becoming an NRI, then such NSCs can be held up till maturity.

- Hindu Undivided Families (HUFs) are not eligible.

- Trusts are not eligible.

- Karta of HUFs, however, can purchase NSC but only in their name.

Benefits of NSC

- Fixed Income: NSC certificates offer fixed interest rates that are decided quarterly by the Finance Ministry. The NSC interest rates are higher than the FD and savings account interest rates. Currently, the National Savings Certificate interest rate is at 6.8% p.a. Hence, this is a guaranteed regular income for you.

- Lock-in period/ Maturity period: The maturity period of the National Savings Certificate is 5 years. This is lower than that of PPF (15 years) and NPS (till retirement).

NSCs were earlier available in 2 tenures: 5 years (NSC VIII) and 10 years (NSC IX). Now, the NSC IX has been discontinued, so only the NSC VIII is available as of now.

- Minimum Investment: The minimum investment allowed in an NSC certificate is INR 100 only. Also, there is no upper limit to investing in an NSC. You can issue an NSC in the denominations of INR 100, INR 500, INR 1000, INR 5000, and INR 10,000.

- Interest Rate: The National Savings Certificate interest rate is currently fixed at 6.8%. The Government revises this figure every quarter. The interest you earn on NSC gets compounded yearly but you will receive the interest at the time of maturity.

- Tax Benefits: NSC Certificate is a government-backed initiative and so you can claim a tax deduction as per Section 80C of the Income Tax Act, 1961 up to an investment of INR 1.5 lakhs.

- Loan Collateral: The banks and NBFCs will accept NSC as a collateral or security in case you take up a secured loan. For this, the postmaster involved will need to put a transfer stamp on the certificate and then transfer it to the bank.

- Power of Compounding: The interest earned on the NSC will get reinvested by default, and this way you will get the benefit of the power of compounding. However, it does not give you high returns that can beat inflation.

- Nomination: You can nominate any of your family members, including a minor. This way the nominee will inherit the NSC amount in case of your demise.

- Accessibility: The government had launched the NSC scheme to keep it accessible to the investors. You can buy it from any post office by submitting all the required documents and the KYC procedure. You can also transfer the NSC from one Post Office to another.

- Maturity corpus: TDS (Tax Deducted at Source) does not apply to the TDS payouts. So, you will be able to receive the entire maturity value.

- Premature withdrawal: NSC schemes generally have a lock-in period of 5 years. You cannot exit early. But, they will accept exceptional cases such as a court order or the investor’s death.

Does NSC come with Tax Benefits?

Image Source: comparepolicy.com

National Savings Certificates do come with Tax Benefits. Investments of up to INR 1.5 lakh will allow you to claim a tax deduction under Section 80C. Also, the interest you receive on these certificates will be eligible for tax benefits as they are added back to the initial investments. The reason being that the interest gets added to the original investment and will be compounded annually.

For example,

If you buy NSC worth INR 1000, then you would be eligible for the tax rebate on the initial investment in the first year. However, you can also claim tax deductions in the second year as the interest earned in the first year gets added to the original investment, hence, compounded annually.

NSC Vs other Tax-Saving Schemes

There are several tax-saving investment options available under Section 80C of the IT Act. NSC certificate is one of the most popular such options. Other tax-saving investment tools include Equity Linked Savings Scheme (ELSS), National Pension System (NPS), Public Provident Fund (PPF), and tax-saving Fixed Deposits (FD).

| Investment | Interest rates | Lock-in period | Risk associated | Compounding frequency | Minimum Investment | Maximum Investment |

| NSC | 6.8% | 5 years | Low-risk | Annually | INR 100 | No upper limit |

| ELSS funds | 12% to 15% | 3 years | Market associated risks | Annually | INR 500 | INR 1.5 lakh per year |

| PPF | 7.1% | 15 years | Low-risk | Annually | INR 500 | INR 1.5 lakh |

| NPS | 8% to 10% | Up till retirement | Market-related risks | Monthly | INR 6,000 per year | INR 1.5 lakh |

| FD | 5% to 7% | 5 years | Low-risk | Quarterly | INR 5,000 | No limit |

NSC Interest Rates

The interest rate of the National Savings Certificate scheme changes periodically as per the Finance Ministry’s decision. This rate is decided quarterly. From 1st July 2020 to 30th September 2020, the NSC Interest rate is at 6.8%. Given below is the NSC interest rate chart that compiles the quarterly interest rates from 2018 to 2020.

Note: The NSC interest is compounded annually. But, all the accumulated interests are payable only at maturity.

| Period | Interest Rate |

| Q1 FY 2020-21 | 6.8% |

| Q4 FY 2019-20 | 7.9% |

| Q1 FY 2018-19 | 7.6% |

| Q2 FY 2018-19 | 7.6% |

| Q3 FY 2018-19 | 8.0% |

| Q4 FY 2018-19 | 8.0% |

| Q1 FY 2019-20 | 8.0% |

| Q2 FY 2019-20 | 7.9% |

| Q3 FY 2019-20 | 7.9% |

How and where to buy NSC?

You can purchase an NSC for yourself, with an adult as a joint account, or on the behalf of a minor. Nowadays NSC online purchase is also available. Before 1st July 2016, physically pre-printed NSC certificates could be issued by post offices or banks. But, now these certificates can be issued in 2 modes:

- Recorded in 2 modes: 1. e-mode (electronic mode), 2. Passbook mode

- You can purchase it from all PSBs (Public Sector Banks) and top 3 Private Banks (ICICI, HDFC, and Axis Banks)

You can also buy National Savings Certificates (NSCs) in e-mode if you have a Savings Account with Bank/ Post Office and net banking access.

Step-by-step procedure to buy NSC

As already stated, you can buy an NSC from any Post Office. Currently, you cannot buy National Savings Certificate online. Given below is a step-by-step guide to buying NSC certificate:

- Get an NSC form from your nearest Post Office and duly fill in the requisite details.

- Submit the documents required

- Fill up the details of the nomination

- Make the payment of the amount you want to invest in the NSC. You can make the payment in any of the following modes:

- Cash

- Cheque

- Pay Order

- Demand Draft

- You can also surrender an old matured NSC and invest the matured amount in a new NSC. But, you need to mention the following on the back of the surrendered certificate:

“Received payment through the issue of a fresh certificate, vide application attached.”

- The Post Office will initiate the verification of your details and documents.

- After successful verification, the NSCs of the amount invested will be printed. You can collect the same from the respective Post Office.

Holding Modes of NSC Certificate

There are 3 different modes through which you can hold a National Savings Certificate. These are as follows:

- Single Holder Type Certificate: The single holder certificate is issued to you for yourself or on a minor’s behalf.

- Joint A Type Certificate: This certificate is held by 2 investors and both will receive an equal share of maturity amount.

- Joint B Type Certificate: This is a type of joint holding certificate but the maturity amount will be paid to only one of the holders.

Documents Required for NSC

For any investment, you need to submit some documents. Likewise, you need to submit certain documents to invest in an NSC which are listed as follows:

- NSC application form

- Original Identification proof which can be any of the following:

- Passport

- Voter ID

- Permanent Account Number (PAN) Card

- Driving license

- Government ID

- Senior Citizen ID

- Aadhaar card

- Photograph

- Address proof which can be any of the following:

- Electricity Bill

- Passport

- Telephone Bill

- Bank Statement along with a Cheque

- Aadhaar Card

When can you withdraw a pre-mature NSC?

NSC has a lock-in period of 5 years. However, under certain special circumstances, premature withdrawals can be permitted:

- If the NSC holder dies

- If a pledgee (who must be a Gazetted Government Officer) issues a forfeiture.

- If the courts issue an order of premature withdrawal of NSC.

NSC Calculator

NSC Calculator is available online and you can download it for free. It uses the following formula to calculate your interest accrued every year and the maturity amount.

NSC Maturity Amount = Amount Invested * (1 + Interest Rate) ^ 5

Through this, you can calculate your maturity amount. Just enter the following details and you are good to go:

- Purchase Amount

- Interest Rate

NSC interest rate calculator is also available. You need to enter the following details in the fields of a National Savings Certificate Interest rate calculator to get the accrued interest amount.

- Interest amount

- Date of purchase of the NSC

FAQs

Q1. What income tax benefits will I get if I invest in post office National Savings Certificate?

Ans. You can avail tax deductions under Section 80C of the IT Act, 1961 for investments up to INR 1.5 lakh. Also, the annual interest you receive from your NSC will be added to the original investment amount and thus, that is also eligible for tax benefits.

TDS is not charged on NSC but you must pay the tax on the interest earned accordingly.

Q2. After how many years does an NSC double?

Ans. The time after which an NSC doubles in amount depends on the investment made and the interest rate.

Q3. What is the current post office NSC interest rate?

Ans. The current quarter’s interest rate is 6.8%. The interest rate is revised quarterly.

Q4. Can we redeem an NSC before its maturity period?

Ans. Yes, you can, but only in certain cases: if the investor dies suddenly, or if the court passes such an order. The maturity period of NSC is 5 years.

Q5. How many NSC can I buy?

Ans. You can purchase as many NSCs as you want. There is no maximum limit but the minimum amount for NSC investment is INR 100.

Q6. Can I make monthly installments in NSC?

Ans. The Government allows you to invest up to 12 installments in a fiscal year as long as the total investment sum does not exceed INR 1.5 lakh.

Q7. Under what circumstances can I issue a duplicate NSC certificate?

Ans. You can issue a duplicate NSC certificate in any of the following cases:

- The original NSC gets lost

- Stolen

- Destroyed

- Defaced

- Mutilated

You just need to fill up the Form NC-29 and submit it at the PO where you issued the original NSC in the first place. You need to fill up the following key fields in the form:

- NSC details such as:

- Serial Numbers

- NSC issue

- Denominations, etc.

- Date of purchase of the NSCs.

Q8. Is NSC a one-time investment?

Ans. Yes, it is. The NSC investment has no maximum limits and you can start it from as low as INR 100.

Q9. Is NSC a safe investment?

Ans. Yes, NSC is a safe investment mode. It offers fixed returns and is ideal for people with low-risk tolerance. Also, it offers tax exemptions under Section 80C of the Income Tax Act, 1961.

Q10. How is the NSC maturity amount paid to you?

Ans. You can en-cash the National Savings Certificate at the PO (Post Office) where you registered it. You can also en-cash the amount at any other Post Office if the Office-In-Charge of that PO receives satisfactory verification from the office where you registered the NSC.

Latest posts by Nirupama Verma (see all)

- What is Corporate Gifting and Why is It Important? - November 8, 2023

- Top 5 Benefits of Synthetic Liquids That You Did Not Know - December 24, 2022

- Pin up Review - September 23, 2022